Article on Proposed Changes to Section 20 Assessed Losses for Companies

/Written by Roulon du Toit

The South African corporate income tax rate is scheduled to decrease from 28% to 27% on 1 April 2022. Yipee.

BUT,

To help fund this change, there is a proposed change to the manner in which companies will be able to utilise assessed tax losses that arose in prior tax years. Currently, a company can set off the balance of assessed losses incurred in prior years against its taxable income with no limitation. The proposed amendment seeks to impose a limit to the number of assessed losses that the company may use.

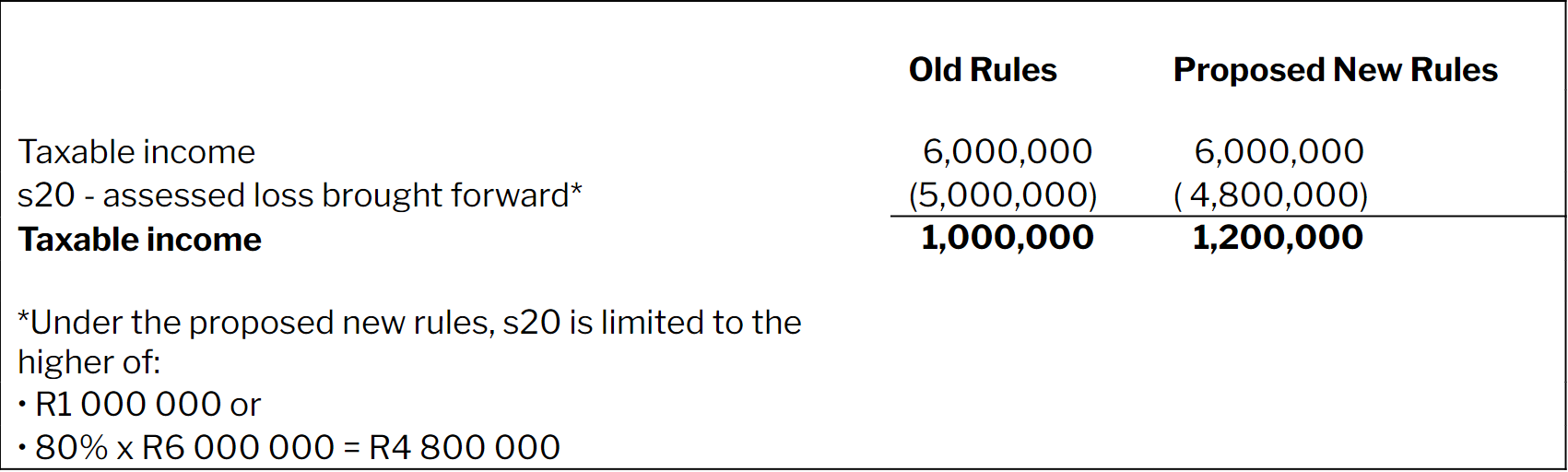

The proposed change to Section 20 indicates that the assessed loss that may be set off against the taxable income of a company may not exceed the higher of

R1 million and

80% of the company’s taxable income before taking into account the assessed loss

For many companies this will mean that they will be taxed on a minimum of 20% of their taxable income generated during a specific year.

If you have an assessed loss, come and chat to us to ensure you understand the new change in the law.

Let’s illustrate the change in an example.

SCENARIO:

X Ltd incurred an assessed loss of R5 000 000 in 20x1. In 20x2 X Ltd calculated a taxable income, before taking into account the prior year’s assessed loss, of R6 000 000.

The taxable income of the company for 20x2 under the old rules and under the proposed new rules is shown below:

Any balance of the assessed loss not used in the current year will be carried forward to the next tax year.

This is effective from the 1st of April 2022.